Home > Faq

FAQ

Your real estate questions answered.

Do you have a question about real estate? You might find the answer on this page.

Didn't find it? Let us know via hallo@habicom.be and we will answer your question as soon as possible.

Do you have a question about real estate? You might find the answer on this page.

Didn't find it? Let us know via hallo@habicom.be and we will answer your question as soon as possible.

Habicom is aangesloten bij de beroepsorganisatie 'Beroepsinstituut van Vastgoedmakelaars - Luxemburgstraat 16B - 1000 Brussel', en als erkend vastgoedmakelaar-bemiddelaar onderworpen aan de BIV-plichtenleer. Habicom treedt op middels in België erkende vastgoedmakelaars BIV onder de nummers: 502 957 – 503 035 – Ondernemingsnummer: 0836.586.396 - BA en borgstelling via NV AXA Belgium - polisnr. 730.390.160 - Derdenrekening habicom – BE96 0688 9938 1805

Om u de best mogelijke ervaring te bieden, gebruiken zowel wij als derde partijen technologieën zoals cookies om toegang te krijgen tot apparaatinformatie en/of deze op te slaan. Door in te stemmen met deze technologieën, stelt u ons en derde partijen in de mogelijkheid persoonlijke gegevens zoals browsegedrag of unieke ID's op deze website te verwerken. U kan uw keuze altijd wijzigen onderaan de pagina via de optie 'cookies' of 'cookie instellingen'.

Instellingen aanpassen

Initially, the buyer must pay transfer tax (also known as registration duties) on every purchase of real estate, unless the property is sold under the VAT system. These registration duties amount to 12% (general) or 3% (in case of a single primary residence and if there is also a promise of energy renovation 1%) of the sales price in the Flemish region.

This amount is paid to the notary at the signing of the authentic deed, who will then transfer it to the competent government authority.

In addition to the aforementioned registration duties, you must also pay the notary's fee. When calculating this fee, no account is taken of the number of hours the notary and/or his staff spend on a specific file. The prevailing rates for drawing up an authentic deed are set in a Royal Decree according to a degressive scale of percentages. This means that the percentage will decrease with a higher purchase price.

The calculation brackets are as follows:

first bracket up to 7,500 EUR: 4.56%

bracket from 7,500 EUR to 17,500 EUR: 2.85%

bracket from 17,500 EUR to 30,000 EUR: 2.28%

bracket from 30,000 EUR to 45,495 EUR: 1.71%

bracket from 45,495 EUR to 64,095 EUR: 1.14%

bracket from 64,095 EUR to 250,095 EUR: 0.57%

bracket higher than 250,095 EUR: 0.057%

You can make the calculation at https://www.notaris.be/rekenmodules/aankoop.

In addition to this amount, the notary must withhold 21% VAT, which he must transfer directly to the federal government. The notary is ethically obliged to comply with these legal scales, so he is not allowed to offer certain discounts or charge a higher fee.

For each purchase deed, the notary must incur some necessary costs, which he will pass on to the buyer. These include costs for conducting certain searches and obtaining the necessary certificates and documents (e.g. soil certificate, mortgage certificate, tax searches, etc.)

Unlike the notary's fee, this amount is not legally fixed and therefore depends on the notary. In addition, the complexity of the file and the rates in your region will also play a role.

Transfer costs: Next, you must also take into account the costs of the transfer. After the authentic deed is drawn up, it is transferred to the mortgage office. This transfer makes the deed opposable to third parties. For this transfer, you can expect to pay around €15 per page.

If you take out a mortgage loan for the purchase of your home, you will incur additional costs. A registration fee must be paid, amounting to 1% of the total amount for which a mortgage is taken, and the mortgage duties must be settled. There is also a fee for documents of €50. For the execution of the deed, the notary will charge a fee that is legally established and varies depending on the loan amount, as is the case with the sales deed. Additionally, he will also charge deed costs, which are costs he had to incur to gather various information.

The general rule is that registration duties (= current sales taxes) are due on the sale of your building land or house. In Flanders, these registration duties amount to 12% (general) or 3% for the sole owner-occupied home, while in Brussels you will pay 12.5% registration duties.

As an exception, a real estate property can be subject to 21% VAT, namely if this real estate property can still be considered as 'new'. There is also a reduced rate of 1% for substantial energy renovations for the sole owner-occupied home.

A house is considered as new construction until December 31 of the second year after the year in which it was first put into use or acquired. For example, if a house is first put into use in March 2015, it is considered as new construction until December 31, 2017.

Whether a house is considered as 'new' depends on the status of the seller. If the seller is a professional (a so-called professional builder), the sale automatically falls under the VAT system. If the seller is a private individual, they have the choice to sell with sales taxes or with VAT.

When purchasing a 'new' house, 21% VAT must also be paid on the accompanying land, provided that the following three conditions are cumulatively met:

If these three conditions are not met simultaneously, VAT will be paid on the construction and registration duties on the value of the land.

When purchasing undeveloped building land, you pay sales taxes on the price of the land, as it cannot be considered as 'new'. However, you can also combine both! Additionally, there is the option to combine registration duties and VAT. When buying a house off-plan or a turnkey house, you can pay registration duties on the purchase of the land and VAT on the purchase price of the house, provided it is a 'yet to be built' house to which the Breyne Law applies. In such a purchase, you become the direct owner of the land, but only later of the house.

However, if you buy a house that is already under construction, the land and the house are sold simultaneously, and the sale will fall entirely under the VAT system.

As a private individual, it is more advantageous to buy under the registration duties system. In the Flemish region, the registration duties amount to 12% of the price.

Therefore, always consider that besides the purchase price, there are additional costs associated with buying a house.

Buyers who significantly energetically renovate OR (partially) demolish or rebuild their home enjoy a reduced registration fee of 1% if this is also their only own home. However, there are a number of conditions:

In addition to the conditions for the reduced rate for the only own home, you must also meet the following additional conditions.

There is a complete reconstruction if a complete demolition of an existing building has been carried out, followed by the construction of a new building.

We speak of a partial reconstruction in the following cases:

the construction of a new building after prior demolition works of a part of an existing building;

which may or may not be combined with the renovation of remaining parts of the existing building;

where the new part

or has a protected volume larger than 800m³;

or contains at least one housing unit;

or a renovation of an existing building, where at least 75% of the partition structures enclosing the total protected volume of the building after the works and bordering the external environment are new.

The works must be related to a 'significant energetic renovation' or a (partial) reconstruction according to the EPB declaration.

In addition, the buyer must meet the EPB requirements stated in the environmental permit for urban planning actions of the construction project. This is also verified through the EPB declaration, which becomes a real control document.

The application of the reduced rate of 1% does not happen automatically. The buyer has two options:

Either the buyer requests the immediate application of the 1% rate in the notarial deed. The notary will provide the necessary mentions.

Or the buyer requests the application of the reduced rate afterwards. In the deed, the reduced rate of 3% can be requested. Once the buyer obtains an EPC-Building, he requests a refund of 2% of the "excess" tax paid from the Flemish Tax Administration (Vlabel).

The electrical inspection is a report that maps out the condition and conformity of the electrical installation(s) in your home. Such an electrical inspection must be carried out by a recognized inspection body.

The inspection report drawn up by a recognized inspection body remains valid for 25 years if it is compliant and provided that no significant changes are made to the installation during this period.

If you want to sell your home and the electrical installation dates from before 1981, it is mandatory to have an electrical inspection carried out. If the result shows that the electricity is not compliant, the buyer will be obliged to rectify the installation and have it re-inspected, they have 18 months from the date of the sales deed to do so.

If the electrical installation dates from after October 1, 1981, a new electrical inspection is not necessary if it is compliant, unless you no longer have the inspection report. In case of a negative inspection report, it is necessary to rectify the infringements and to have a follow-up visit by the same recognized inspection body within a period of 12 months from the date of the initial inspection visit (this can be done by either the buyer or the seller).

The EPC is a certificate that indicates the energy efficiency of your home.

On this certificate, you can read an EPC figure: this number expresses how much energy a home consumes per square meter per year. The lower your EPC figure, the better your home's energy score is.

An EPC must be prepared by a certified energy expert. This expert conducts a comprehensive survey in your home to determine its energy score. The energy expert takes into account various factors such as the condition of the heating system and/or boiler, the presence of solar panels, wall and roof insulation, the type of glazing, the orientation of your home, etc.

An EPC is valid for ten years in principle. For example, if you resell or rent out your home 5 years after the EPC was prepared, a new EPC does not need to be issued unless significant energy-saving works have been carried out on the property that would significantly affect the energy score of your home.

Only EPCs issued from 2019 onwards are eligible for the sale of a property. Valid EPCs for construction, issued with an EPB declaration, before 2019 can still be used for sale.

For rentals, EPCs issued before 2019 that are still valid at the time of signing the lease agreement can still be used.

Properties built with a building permit issued after January 1, 2006, must meet strict energy requirements. For such properties, an EPB file must be prepared when building. EPB stands for 'energy performance and indoor climate'. The file describes to what extent the (new) property meets the legal requirements regarding thermal insulation, energy performance, and ventilation.

Therefore, the EPB file is more comprehensive than an energy performance certificate and provides potential buyers or tenants with additional information. Like the EPC, an EPB file is valid for ten years in principle.

Although the content of the EPC is purely informative, you cannot sell your home today without having an EPC for the property. The buyer must be informed in advance about the energy consumption of the property: such information can play a role in the decision to purchase or in determining the price. The EPC score of the property must already be mentioned at the start of the sales publicity. The original energy performance certificate must be provided to the buyer no later than the signing of the private sales agreement (compromise).

Just like for sales, as a landlord, you must also have a valid EPC certificate in order to rent out a property. The tenant also has the right to know the energy consumption of the property before the lease agreement is concluded. The EPC score of the property must already be mentioned at the start of the rental publicity. If the tenant wishes, they can always obtain a copy of the energy performance certificate at the signing of the lease agreement.

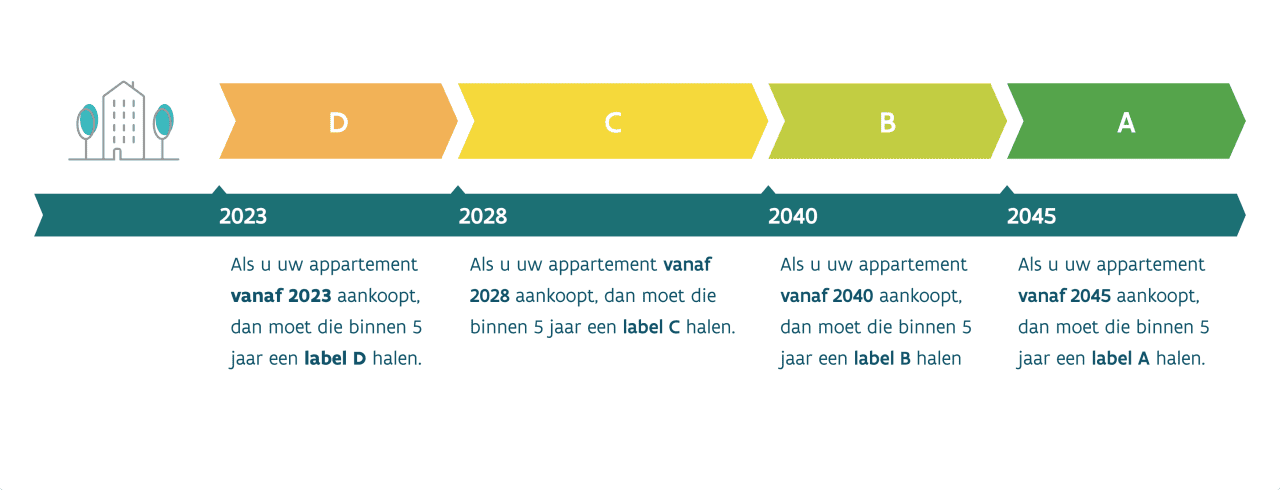

Since January 1, 2023, the retrofitting obligation applies to residential buildings. All homes and apartments purchased from 2023 with an E or F label must be renovated to a D label or better within 5 years of purchasing the property. This must be proven with a new EPC certificate.

The retrofitting obligation applies:

when authentic deeds of a notarial transfer in full ownership, such as a purchase, donation, etc., are drawn up, when establishing a building right or establishing a leasehold for the actual condition at the time of drawing up the deed or establishing the building right or leasehold. If the unit has a residential purpose at the time of transfer, the retrofitting obligation for residential buildings applies. It does not matter what the future plans are for the property.

The 5-year period starts on the date of the authentic deed or on the date of establishing the building right or leasehold.

Label D is a first step towards a larger vision. Label A is the ultimate goal for every home or apartment by 2050. The long-term path has been defined with stricter regulations in 2028, 2035, 2040, and 2045.

The soil certificate is a report that provides information about the soil quality of a specific plot of land. This certificate is issued by OVAM (the Public Waste Agency).

OVAM will inform through the soil certificate whether the plot of land is included in its database of contaminated grounds. If the plot of land is not known in OVAm's database, you will receive a so-called 'blank' soil certificate.

Attention! This does not mean that the soil cannot be contaminated, but only indicates that OVAM has no knowledge of any contamination on this plot of land.

A plot of land (whether built on or not) cannot be transferred or sold without a valid soil certificate. Although the content of the certificate is purely informative, the sale cannot proceed without approval from OVAM.

At the latest when the sale of a property is finalized (usually at the signing of the private sales agreement or compromise), the buyer must have been informed of the content of the soil certificate so that they are aware of the soil condition of the property to be purchased.

The soil certificate must be requested from OVAM. The request can be made in writing or digitally. Generally, the request for the soil certificate should be made by the seller and at their expense.

If the soil certificate indicates that there may have been a risk activity, such as environmental pollution or the presence of a large oil tank, on the plot of land, an initial soil investigation is required. This investigation is carried out by a recognized soil remediation expert, who takes soil samples and analyzes them to determine any contamination. The report of the soil remediation expert is submitted to OVAM. If OVAM concludes after the initial soil investigation that there is no contamination, the transfer can proceed.

If contamination is found, the soil remediation expert continues with their work. This involves conducting a detailed descriptive soil investigation, mapping out the contamination in detail, and potentially drafting a remediation plan. OVAM then decides after analyzing this detailed report whether remediation works are necessary and who is responsible for them.

At that point, the buyer and seller must make further agreements regarding the execution and costs of these works, resulting in the initiation of a soil remediation project. Only after these works have been carried out (during the soil remediation project or upon its completion) can the transfer of the plot of land take place.

An asbestos certificate is the result of an asbestos survey of a building. Based on this survey, OVAM issues a unique asbestos certificate for each building. This certificate contains information about asbestos in the building and assesses whether it is asbestos-safe. It describes for normal use of the building:

An asbestos certificate is mandatory in the case of a transfer between living persons, to a new owner, of an accessible structure that was built before 2001.

For an accessible structure (built before 2001) that is smaller than 20 m², the asbestos certificate is not mandatory, except if:

The asbestos certificate must be present at the time of the transfer agreement. This is usually the compromise, but it can also take place at another time.

The notary can always determine on a case-by-case basis whether an asbestos certificate is necessary and at what point it must be available.

Starting in 2032, for every accessible structure built before 2001 of which you are the owner, an asbestos certificate will be mandatory, even if you have no plans for a transfer.

Currently, renting in itself is not a reason to have an asbestos certificate drawn up. But if an asbestos certificate is available, you are obligated to provide a copy to the tenant(s).

To obtain an asbestos certificate for your property, appoint a certified asbestos expert for the survey. On the OVAM website, you can find a list of companies authorized to conduct an asbestos survey for the asbestos certificate (opens in a new window). You can search by name or by municipality and postal code. This list is updated at least weekly.

As the owner, you can also grant power of attorney to have an asbestos certificate drawn up, for example to a notary, real estate agent, or building manager.

A group of recognized assisted living apartments consists of one or more buildings, where seniors aged 65 and older live with their partner or alone in individually adapted apartments and where they can rely on professional care services. If their need for care suddenly increases, they can stay in their familiar environment. All services can be provided at home.

An appointed management authority organizes all care and services, provides a 24/24 emergency call system, and even takes on the management of the buildings in some projects. A residential assistant is present at fixed times. This man/woman is a confidant and listening ear, who assists you in finding a cleaning aid and/or hairdresser and helps you with your administration. The residential assistant arranges everything for you.

Only 'recognized' assisted living apartments by the Agency for Care and Health can benefit from special tax advantages. As a buyer, you only pay 12% VAT instead of 21% VAT on the construction. You are also exempt from property tax.

A certified assisted living complex consists of one or more buildings, where seniors aged 65 and older can live alone or with their partner in individually adapted apartments. Here, they have access to professional care services and can, if necessary, stay in their familiar environment as their care needs change. All necessary services can be delivered to their home.

A designated management authority coordinates all care and services, including a 24/24 emergency call system, and in some cases even takes over the management of the buildings. At set times, a residential assistant is available, who acts as a confidant and listening ear. They can help with finding household help and/or a hairdresser, and provide support with administrative tasks. The residential assistant handles all matters for the residents.

Only assisted living facilities that are recognized by the Agency for Care and Health can benefit from special tax advantages. As a buyer, you enjoy a reduced VAT rate of 12% instead of 21% on the construction, and you are also exempt from property tax.

When you make an offer - whether it is done verbally, via email, through a text message, or by letter - you are always entering into a commitment. If the seller accepts your proposal, you must buy the house for the amount you have offered. If you have been too hasty and ultimately do not want to buy the property, you can, but the seller then has the right to claim compensation, usually amounting to 10% of the agreed price.

A text message can also serve as evidence in the purchase or sale of a property. The Court of First Instance in Ghent stated in 2012 that 'a text message is not an informal sales agreement or compromise, but a document that can serve as the beginning of proof.' To ensure your purchase, it is always advisable to put your agreements in writing and to be guided by your notary or real estate expert.

Contrary to movable goods, Belgian real estate can never be gifted for free. Fortunately, the current gift tax has recently been reduced and simplified.

Donation of real estate must always be done through a notary. The notary will draw up a notarial deed, which must be registered no later than fifteen days after the notarial deed of donation. As a result, you are liable for gift tax (the so-called 'donation rights').

The applicable rates ('gift tax') depend on the relationship between the donor and the beneficiary on one hand, and the value of the real estate on the other hand.

The rates applicable in Flanders in direct line (= child, grandchild, ...) or between spouses/cohabitants are as follows:

Bracket from 0 to 150,000 EUR: 3%

Bracket from 150,000 EUR to 250,000 EUR: 9%

Bracket from 250,000 EUR to 450,000 EUR: 18%

Bracket > 450,000 EUR: 27%

The rates applicable for donations between other persons (e.g. nephew, aunt, ...) are as follows:

Bracket from 0 to 150,000 EUR: 10%

Bracket from 150,000 EUR to 250,000 EUR: 20%

Bracket from 250,000 EUR to 450,000 EUR: 30%

Bracket > 450,000 EUR: 40%

If the beneficiary decides to make energy-saving investments in the donated property, there is a possibility to receive an additional discount on the gift taxes. You can consult the exact rates on the website of the Flemish tax authorities.

In the Flemish Region, there is an exemption from gift tax for the donation of family businesses and companies. The purpose of the scheme, which has been in effect since January 2012, is to encourage business owners to think about their succession during their lifetime.

There are various conditions that must be met, both before and after the donation. You must also fulfill certain formalities. Therefore, be sure to seek advice on this matter!

Costs refer to the expenses made to enable the tenant to fully enjoy the leased property or to enhance this enjoyment. Some examples include the provision of gas, electricity, heating, and water.

Charges include the taxes and levies paid to the government. Examples of these are the garbage tax and the property tax.

Regarding the distribution of these costs and charges between tenant and landlord, there has often been discussion in the past. The Flemish Housing Rental Decree has attempted to end these discussions. For lease agreements concluded in Flanders from January 1, 2019, there is a clear regulation on which costs and charges can be passed on to the tenant by the landlord.

In general, costs and charges are divided as follows:

Landlord: repairs of damage caused by force majeure or wear and tear.

Tenant: maintenance and minor repairs.

To clarify this distribution and prevent disputes between landlords and tenants, the Flemish Government has drawn up a non-exhaustive list of minor rental repairs. It has also been confirmed that the property tax cannot be passed on to the tenant.

Furthermore, for apartments and houses that are part of a co-ownership, an additional non-exhaustive list has been drawn up, clearly determining the distribution of common costs between tenant and landlord. This makes it clear which common costs the landlord can pass on to the tenant.

This list is included in Annex 2 of the Implementation Decree of December 7, 2018, related to the Flemish Housing Rental Decree and determines as follows:

|

Multi-family dwellings |

For the tenant |

For the landlord |

|

1. Water consumption |

? |

|

|

2. Fuel oil/natural gas consumption |

? |

It is important to note that the landlord and tenant cannot deviate from this regulation in principle, although it will be allowed for the landlord to incur additional costs and charges in favor of the tenant.

In the case of commercial lease or general lease, it is possible to determine in the lease agreement who bears the costs and charges. If no agreements have been made, the principle applies that only costs and charges related to services or performances from which the tenant benefits can be passed on to the tenant. This includes energy supply, maintenance of common areas such as heating and lighting, and waste costs.

Costs directly related to the ownership of the property, such as property tax, are the responsibility of the landlord. However, it is common for such costs to be contractually assigned to the tenant, which is possible in the case of commercial lease or general lease, unlike residential lease.

Sometimes there are situations where both tenant and landlord benefit from certain costs or charges, in these cases, the costs are shared between both parties.

There are two options:

Costs and charges can be determined on a lump-sum basis. It is important that this is stipulated in the lease agreement to prove the agreement of both parties. The lump-sum amount does not have to correspond to the actual expenses and is not subject to dispute.

If no lump sum has been established, the costs and charges imposed on the tenant must correspond to the actual expenses. These costs and charges must be listed separately in an account, with the landlord providing the tenant with a detailed breakdown of the different costs and the corresponding evidence. Parties cannot contractually exclude this obligation.

Often, the lease agreement stipulates that the tenant pays advances periodically, for example, by transferring a provision to the landlord monthly.

It is crucial that all obligations and agreements between co-owners are documented in writing within a community of co-ownership. This way, everyone has a clear understanding of their rights and responsibilities regarding the building. The main documents for this purpose are the deed of division, the regulations of co-ownership (together known as the articles of association), and the internal regulations. Below you will find more information about the regulations of co-ownership.

The regulations of co-ownership are part of the articles of association of the apartment building or business complex and are drawn up by the notary, together with the deed of division. These regulations determine the main rules for co-owners, both in their relationships with each other and with the Association of Co-Owners (VME).

Co-owners have rights and obligations regarding both the private and common areas.

Each co-owner has "an exclusive and undivided ownership right" with regard to their own private area. However, this right is limited by the interests of other co-owners, as stipulated in the regulations of co-ownership. For example, although a co-owner is generally free to modify or merge their private area, restrictions may be imposed to maintain the appearance of the building.

Each co-owner may make minor changes or improvements within their own private area, but for interventions that affect the common areas, permission from the general meeting is usually required.

The regulations of co-ownership usually also contain clear regulations regarding the use of private areas, such as restrictions on commercial use.

Co-owners share ownership rights over the common areas of the building. The regulations of co-ownership clearly define the permitted use of these common areas.

Criteria for the distribution of costs

The regulations of co-ownership specify how the common costs are divided among the different private areas, which forms the basis for the syndic to distribute the costs among co-owners.

Tenants must also be informed of and comply with the regulations of co-ownership. Landlords must inform tenants of the contents of these regulations before signing the lease agreement and ensure they agree to them. This can be done by adding the regulations to the lease agreement.

As a landlord, you are responsible for informing your tenant about the regulations of co-ownership. If the tenant does not comply with the rules, other co-owners may hold you liable for this.

The annual general meeting of an Association of Co-Owners (VME) is a crucial gathering for owners of apartments or business complexes within the VME. During this meeting, all co-owners come together to discuss and make decisions regarding the co-ownership.

Topics that are addressed include the necessity of renovation works, the selection of a gardener for the maintenance of common areas, the appointment of members of the co-ownership council, and the approval of the annual accounts.

The syndic is legally obligated to convene this meeting annually. In urgent cases, a special general meeting can also be organized. The syndic must convene a special general meeting at the request of co-owners who own at least ? of the shares in the common areas.

In addition to the syndic, other parties such as co-owners, the co-ownership council, or the justice of the peace, can also take the initiative to convene a general meeting in certain cases.

The invitation to the meeting must reach all co-owners at least fifteen days before the date of the meeting, and must include the agenda and the topics to be discussed. Non-voting residents must also be informed of the meeting so that they can submit their comments on the common areas in writing.

During the meeting, all co-owners have voting rights, depending on their share in the common areas. To be valid, more than half of the co-owners must be present and own at least half of the shares in the common areas, unless more than ¾ of the shares are present at the start of the meeting. Decisions are recorded in the minutes, which are signed by the chairman, the secretary, and the co-owners present.

The rent price is generally fixed for the entire duration of the contract. In case of a contract extension, the rent price should remain the same. If there is a short-term contract and the tenant wishes to sign a new contract, the rent price should be the same as in the initial contract.

For all rental agreements, the rent price can be adjusted at fixed intervals. Tenant and landlord can always adjust the rent price between the 9th and 6th month before the end of a 3-year period. If they do not reach an agreement, a petition can be filed with the justice of the peace.

If the landlord proves that the rental value of the property has increased by at least 10% due to renovations, or if the tenant or landlord can prove that the rental value has decreased by at least 20% due to circumstances, the judge can revise the rent price with an increase or decrease that he deems fair.

For rental agreements signed since January 1, 2019, the rent price can also be adjusted at any time if the landlord has carried out energy-saving measures in the rental property.

The rent price cannot be adjusted during the duration of a rental contract. However, the owner can index this rent price. This way, the amount is adjusted to the cost of living increase.

Is rent indexing automatic?

No, rent indexing in Belgium is not automatic. The landlord must take the initiative each year to index the rent. However, the right to index must be mentioned in the rental contract.

The owner must notify the tenant in writing of the rent price indexation on the anniversary date of the rental agreement. This is the date on which the contract came into effect.

If the landlord forgets to timely inform the tenant of the indexation, he still has three months to do so. The indexation can be applied retroactively to the past three months. After this period, he can only claim adjusted rent for a maximum of three months.

The indexing of rent prices in Belgium is calculated using the following formula:

(Base rent x New index) / Start index

Or very easily via the following link: https://statbel.fgov.be/nl/themas/consumptieprijsindex/huurcalculator